(Bloomberg) — In just eight days, China regained the influence it lost over 10 months in emerging markets.

Most Read from Bloomberg

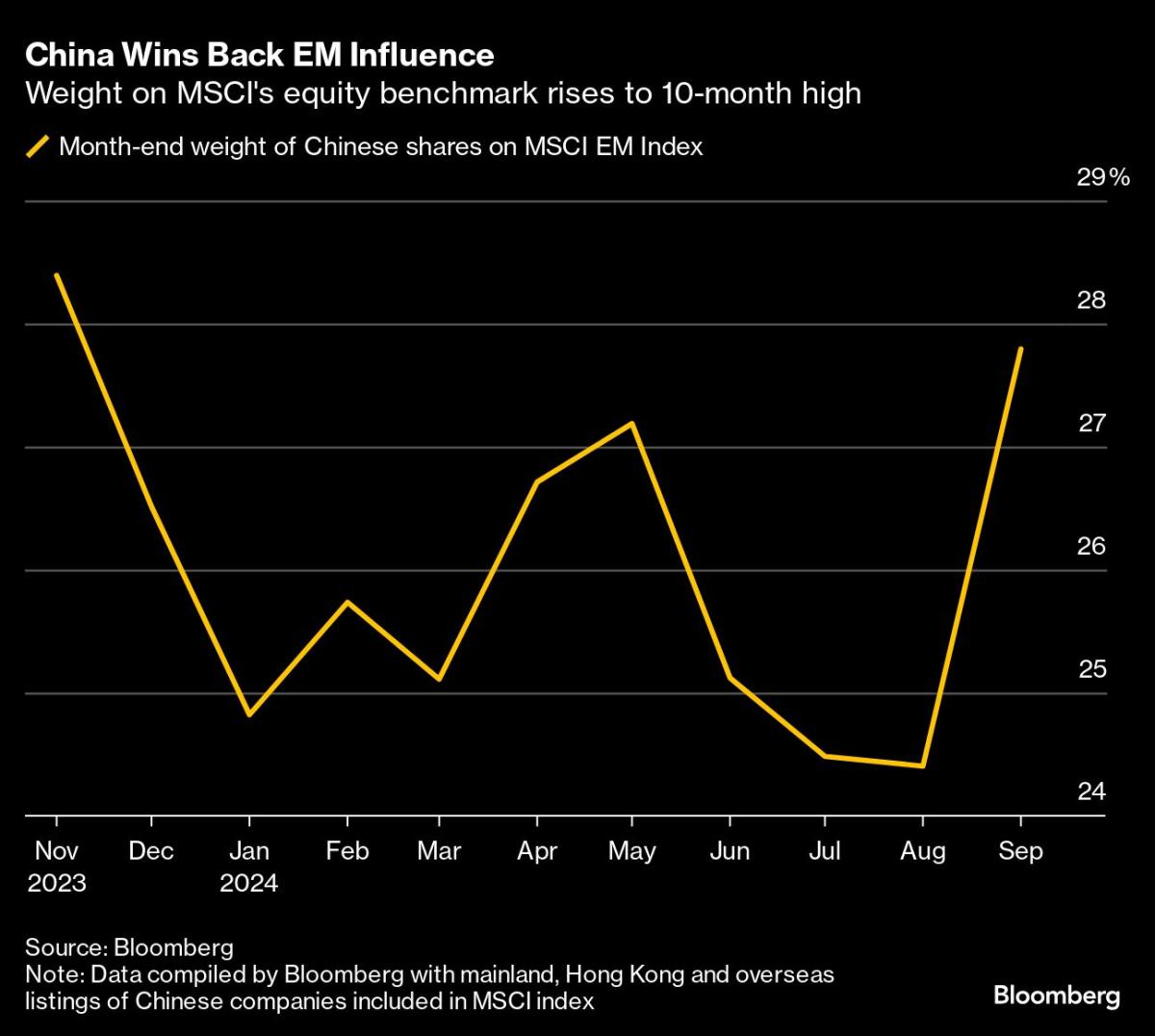

The country’s weight in MSCI Inc.’s benchmark for EM equities climbed back to 27.8% at the end of September, the highest level since November 2023, before the country’s markets closed for a long holiday on Tuesday, according to data compiled by Bloomberg based on the gauge’s shares listed on mainland, Hong Kong and overseas markets.

The increase in China’s weighting was powered by a $3.2 trillion rally in its stocks since Sept. 18, when the Federal Reserve gave a green light to global monetary easing and China followed up with a stimulus bazooka. The stunning turnaround ends a phase in which Chinese stocks were the laggard in emerging markets, losing share in index weights month after month as rival markets such as India, Taiwan and South Korea surged ahead.

Amid deepening outflows and an underperformance that took China to a record low versus the rest of EM, global money managers increasingly started reducing exposure to the country. From Morgan Stanley to HSBC Holdings Plc and Pictet Asset Management, the ranks of China skeptics swelled. Amid the gloom, though, a small band of investors remained faithful to bullish China calls — touting the possibility of greater stimulus as well as cheap valuations. The past few days seem to have validated them.

“It is against the back of very low valuations that this ferocious move up has happened,” said Hasnain Malik, a strategist at Tellimer in Dubai. “It was a folly to think of emerging markets ex-China, given its size, links with the rest of EM, and its cheap valuation, unless sanctions prohibit allocating assets there. This episode, which will have ruined the relative performance of some funds in the third quarter, proves that.”

China’s charge back into the top of the emerging-market leaderboard has been led by mainland stocks, with the benchmark CSI 300 Index soaring 27% since the Fed rate cut. That helped the country beat other emerging markets last month by the most since June 2022.

The gains came after China unleashed a barrage of measures to support the economy and markets. Apart from interest-rate cuts, the central bank established a swap program for financial institutions and introduced a special re-lending facility encouraging buybacks — direct, targeted measures aimed squarely at the stock market. The moves were followed by pledges from the Politburo for deeper stimulus.

Some investors caution against overstating the magnitude of China’s gains.

The rally came off a low base both in terms of valuations and relative performance. Chinese stocks underperformed the rest of EM for four years and sunk to a record low in relative terms just before the Fed move on Sept. 18. Even after this recent rally, they have barely recouped 16% of that underperformance — still leaving a vast gap in returns over the past four years.

The Hang Seng China Enteprises Index’s valuation — the multiple of price over estimated earnings — remains under 10. And the gauge still trades at a 44% discount to the rest of emerging markets, compared with the 15% discount it traded at two years ago.

“The Chinese stock market is still holding single-digit valuations despite these gains, leaving significant room to catch up to the five-year average valuations of 11 to 12 times,” said Aarthi Chandrasekaran, head of asset management at Shuaa Capital, which maintains a neutral stance on China. “For the rally to be sustainable, we need to see improvements in resumption of consumption, housing-sector activity, and a reduction in deflationary pressures. Additionally, the government needs to address the labor market.”

China’s improving fortunes are having other impacts on emerging markets, underscoring the country’s importance to the overall asset class. South Africa’s equity markets completed seven successive months of gains, their longest streak since May 2021, partly on optimism that Chinese stimulus will help drive demand for the country’s exports to the world’s second-biggest economy.

Still, an absence of gains in areas like consumer demand could bring back skepticism on China, leaving the outlook for broader emerging markets dependent on successful implementation of the stimulus. While authorities have demonstrated a commitment to provide support to the economy and equity markets, further measures are needed, Malik of Tellimer said.

“We have not actually seen the sort of fiscal stimulus for consumers that fixes the biggest structural weakness in the macroeconomy,” he said. “Fundamentally, we’re not out of the woods.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Read the full article here

")