(Bloomberg) — Treasury yields tumbled after data showing a further slowdown in the US labor market fueled Wall Street bets on Federal Reserve rate cuts.

Most Read from Bloomberg

Just a few days ahead of the payrolls report, a reading on job openings trailed estimates and hit the lowest level since 2021. The figures sparked an immediate reaction in the bond market, with yields dropping across the board. Shorter maturities led the move. Fed swaps priced in over 100 basis points of policy easing before the year is over — including a jumbo-sized reduction.

Listen to the Bloomberg Daybreak Europe podcast on Apple, Spotify or anywhere you listen.

A key segment of the curve briefly turned positive, an indication to some the economy is on the cusp of a downturn. The “disinversion” restored — for a moment — the “normal” relationship between two- and 10-year yields. Longer-dated ones reflect bets on how the Fed rate will affect growth, and inversions have been harbingers of recession.

“The markets may not be as nervous as they were a month ago, but they’re still looking for confirmation the economy isn’t cooling off too much,” said Chris Larkin at E*Trade from Morgan Stanley. “So far this week, they haven’t gotten it.”

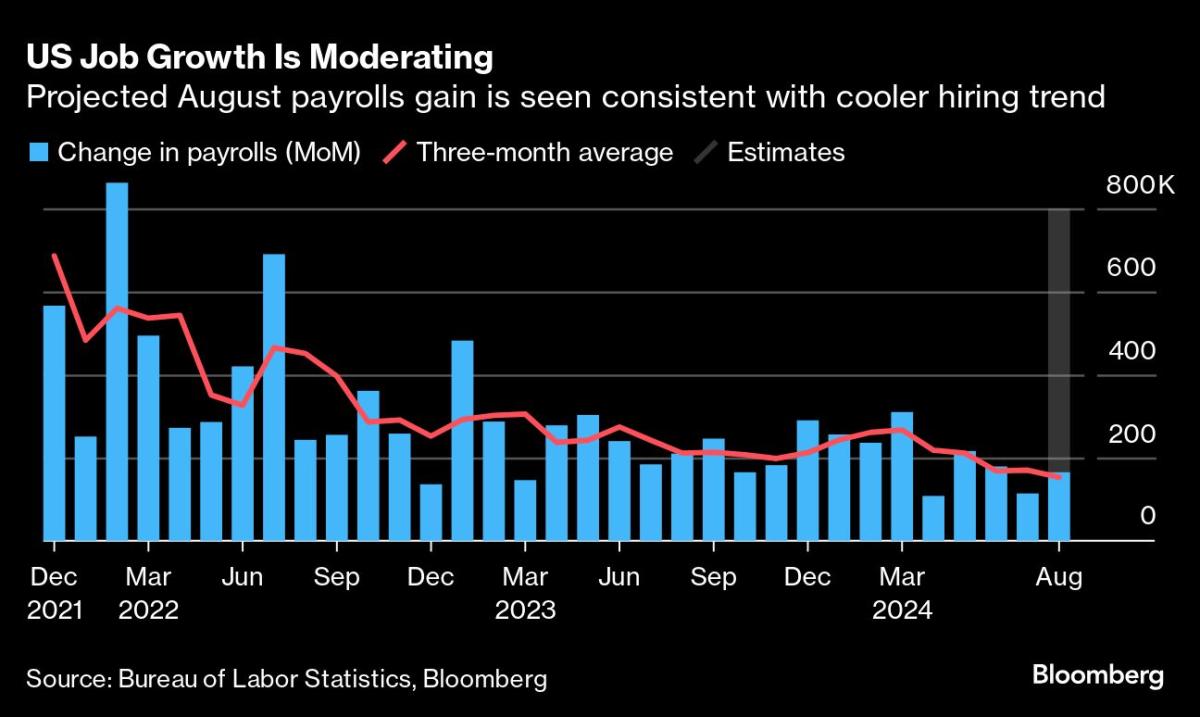

With the Fed set to begin cutting rates in a few weeks, the main question now is how big the first reduction will be. Monthly US employment data due Friday will probably determine the answer.

Investors are on the edge of their seats after the release of the jobs report last month stoked growth fears. Jerome Powell has made it clear the Fed is now more concerned about risks to the labor market than inflation, and another bad report would bolster the case for an outsize rate cut.

“Markets seem to see September as a coin flip between 25 and 50 basis points,” said Neil Dutta at Renaissance Macro Research. “I think going 25 bp risks the same market dynamic as skipping the July meeting. It’ll be fine until the next data point makes investors second guess the decision, fueling bets the Fed is behind the curve. Go 50 when you can, not when you must.”

Treasury 10-year yields declined four basis points to 3.79%. The dollar retreated. The S&P 500 wavered. Nvidia Corp. rebounded after a rough start to September.

The Japanese yen climbed 1%. The loonie underperformed most developed-world currencies after the Bank of Canada cut rates, and reiterated that it’s “reasonable” to expect more easing to come if inflation keeps decelerating.

“Any hint of labor-market weakness has a very large impact on rates and Fed cut expectations, given how focused Powell is on the labor market. So we get the rates market reaction, but it is all about payrolls this week,” said Dennis DeBusschere at 22V Research.

This coming Friday, the August jobs report is expected to show payrolls increased by about 165,000, based on the median estimate in a Bloomberg survey of economists. While above the modest 114,000 gain in July, average payrolls growth over the most recent three months would ease to a little more than 150,000 — the smallest since the start of 2021.

To Krishna Guha at Evercore, the latest job openings figures have come in “on the soft side” overall, but they do not suggest any rapid deterioration in the labor market.

“The still low level of layoffs and tick up in hires suggests the labor market is not cracking,” said Guha. “On net, we think JOLTS nudges down the bar for what the employment report Friday would need to deliver in order for the Fed to cut 50bp out the gates in September, though not radically.”

A stock-market correction may start to “get traction” if Friday’s payrolls report comes in weak, according to Goldman Sachs Group Inc.’s Scott Rubner.

Rules-based systematic funds such as Commodity Trading Advisers, or CTAs, have now asymmetric skew to the downside over the next month. “This is the last week for unemotional demand,” Rubner wrote.

Bank of America Corp. clients were net sellers of US equities for a second consecutive week, recording the biggest net sale of shares since late 2020 as uncertainty grows around the economic outlook.

Institutional, hedge fund, and retail clients all offloaded US stocks, with net sales totaling $8 billion in the week ended Aug. 30, quantitative strategists led by Jill Carey Hall said Wednesday in a note.

Traders Pile Into US Wagers Targeting 10-Year at 4.05% by Friday

Bond traders are bracing for wilder market swings in the US than in Europe amid signs the world’s largest economy is faltering.

A measure of volatility in US rate markets over the coming month rose to the highest since July 2023 on a closing basis on Wednesday. In contrast, the equivalent euro-area metric has been little changed on the week, with the European Central Bank widely expected to cut rates by a quarter point.

Kristina Hooper at Invesco expects the Fed will cut only 25 basis points, but anticipates that would only be the start of what is likely to be a “very significant easing cycle.”

Citigroup Inc. strategists see risk/reward attractive to position for a selloff in US rates via payer options, strategists including Jabaz Mathai and Jason Williams say in a note.

“Our general view on yields is that the market has more room to cheapen from here given that the most recent data are not suggestive of much weakening in activity, but we’ve been less inclined to sell outright.”

Corporate Highlights:

-

Uber Technologies Inc. is tapping the US investment-grade bond market for the first time since it attained blue-chip status.

-

Lyft Inc. plans to write down some of its bike and scooter rental assets, and cut 1% of its employees as the ride-hailing company struggles to turn profitable.

-

United States Steel Corp. is warning union leaders and politicians pushing to block its $14.1 billion acquisition by Nippon Steel Corp. that doing so would imperil thousands of jobs and its Pittsburgh headquarters.

-

Centene Corp. released a projection for members in its Medicaid program that disappointed investors.

-

The Nordstrom family is looking to take their namesake department store chain private in a proposed $3.8 billion deal.

-

Dollar Tree Inc. lowered its full-year guidance as its higher income customers also begin to pull back on spending.

-

Dick’s Sporting Goods Inc.’s higher full-year forecast failed to match expectations for a more sizable upgrade — a repeat of Foot Locker Inc.’s experience last week.

Key events this week:

-

Eurozone retail sales, Thursday

-

US initial jobless claims, ADP employment, ISM services index, Thursday

-

Eurozone GDP, Friday

-

US nonfarm payrolls, Friday

-

Fed’s John Williams speaks, Friday

Some of the main moves in markets:

Stocks

-

The S&P 500 was little changed as of 12:47 p.m. New York time

-

The Nasdaq 100 rose 0.2%

-

The Dow Jones Industrial Average was little changed

-

The MSCI World Index fell 0.4%

Currencies

-

The Bloomberg Dollar Spot Index fell 0.3%

-

The euro rose 0.3% to $1.1077

-

The British pound rose 0.2% to $1.3142

-

The Japanese yen rose 0.9% to 144.12 per dollar

Cryptocurrencies

-

Bitcoin rose 0.2% to $58,357.16

-

Ether rose 0.5% to $2,476.25

Bonds

-

The yield on 10-year Treasuries declined five basis points to 3.78%

-

Germany’s 10-year yield declined five basis points to 2.22%

-

Britain’s 10-year yield declined five basis points to 3.93%

Commodities

-

West Texas Intermediate crude fell 0.9% to $69.73 a barrel

-

Spot gold rose 0.1% to $2,495.88 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Vildana Hajric.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Read the full article here