(Bloomberg) — While the stock market rallied after the long-awaited Federal Reserve rate cut last week, there’s a sense of unease accompanying the gains.

Most Read from Bloomberg

Referring to the Fed’s shift to a bigger rate cut than had been expected even a week before the meeting, Charlie McElligott, cross-asset strategist at Nomura Securities, wrote in a note that the “‘fear of left-tail’ then self-fulfills the right-tail outcome” and that it’s “pushing the market out of recession trades, instead capitulating back into soft-landing” expectations.

That change in market perception is in turn causing a forced re-risking and exposure grabbing, according to McElligott. Some is mechanical, with leveraged exchange-traded funds buying across products, while market-overwriting funds are forced to snap back up short call positions. Other investors who reduced risk after the August volatility spike now have to purchase at record highs — an uncomfortable prospect with a hotly contested presidential election, an uncertain macroeconomic picture and corporate earnings approaching.

“A big re-positioning ultimately sets the table for the next wobble,” says McElligott, adding that more risk taking at some point necessitates downside hedging, which in turn changes the options market’s dealer positioning into something that acts as “accelerant fuel for ugly market events.”

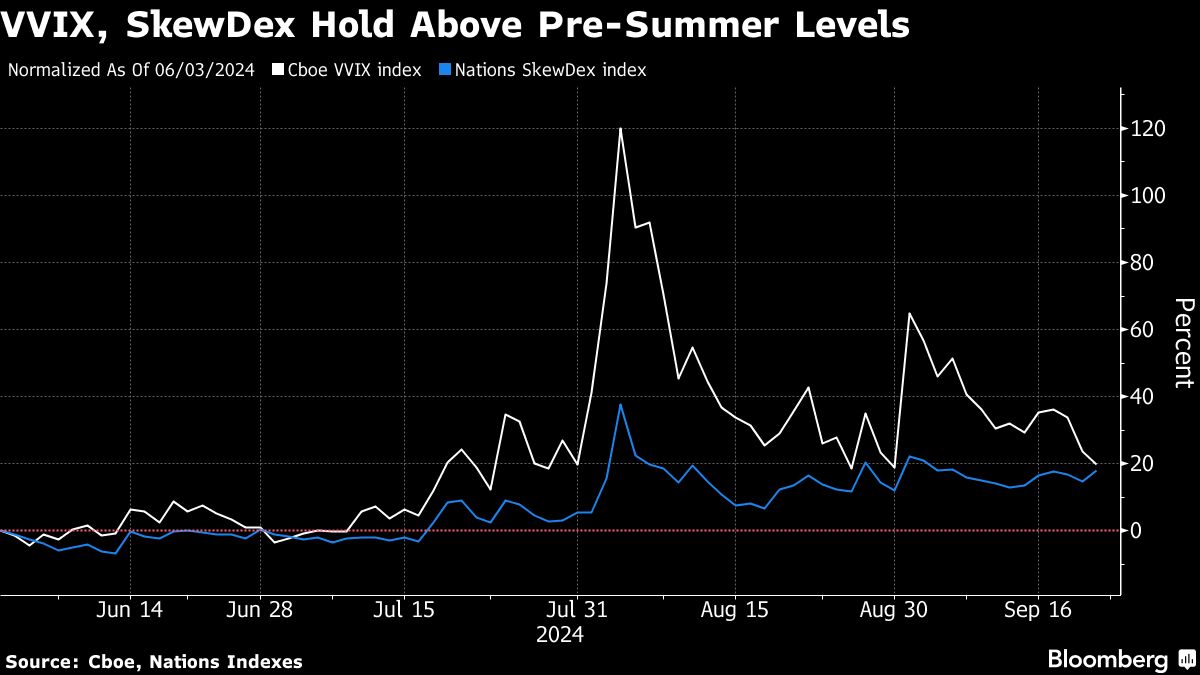

There are signs of that hedging in measures of volatility and skew, signaling that despite US equity gauges rallying to record highs after the Fed decision, investors are willing to pay more for protection. The Cboe VVIX Index — measuring the volatility of VIX options commonly used to guard against a steep selloff — remains about 20% above its level from the beginning of June. And Nations SkewDex, which gauges the relative cost of bearish put options, is also elevated.

In other signs of tail-risk hedging, investors picked up buying of Cboe Volatility Index calls and call spreads — purchasing 85 and 90 calls in particular — and of S&P 500 Index (^SPX) put spreads. Going into the Fed meeting, non-commercial net-short VIX positions were the smallest since 2019.

A pickup in hedging — while protecting individual investors — may leave options dealers short gamma, forcing them to sell more to stay balanced in a sharp market drop.

The central bank’s half-point rate cut raised the question of whether the Fed’s hand had been simply forced, if the market’s big fear of a hard landing, best expressed during the August selloff, was scary enough for policymakers to make a big cut and reassure the soft landing narrative.

And while all the technicalities of the market play their own game, the debate about how low rates can go and how stimulative a cut actually is has just begun.

“We continue to believe that central banks will have less leeway to ease in 2025 than they and many investors believe,” wrote Berenberg economist Holger Schmieding. “Continued loose fiscal policy, persistent underlying inflation pressure and structural labor shortages are reasons against cutting rates too deeply.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Read the full article here

")