Warning: Team Sounds the Alarm")

OCTOBER US INFLATION KEY POINTS:

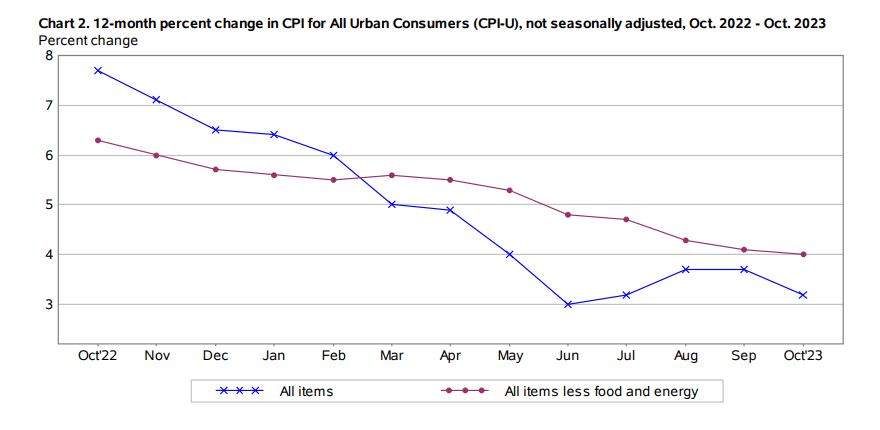

- October U.S. inflation clocks in at 0.0% month-over-month, bringing the 12-month reading to 3.2% from 3.7% previously, one-tenth of a percent below expectations in both cases

- Core CPI increases 0.2 % m-o-m and 4.2 % y-o-y, also below estimates

- Lower than expected inflation numbers will give the Fed cover to embrace a less hawkish stance

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter

Most Read: US Dollar Setups: USD/JPY, GBP/USD and AUD/USD, Volatility Up Ahead

Inflation in the U.S. economy softened last month thanks in part to the Fed’s hawkish hiking campaign and interest rates sitting at multi-year highs, a sign that policymakers are making progress in their quest to restore price stability.

According to the U.S. Bureau of Labor Statistics, the consumer price index was unchanged in October on a seasonally adjusted basis, with the flat reading facilitated by a 2.5% drop in energy costs. This brought the 12-month pace down to 3.2% from 3.7% previously, representing a slow but welcome improvement for the Fed, which targets an inflation rate that averages 2% over time.

Economists surveyed by Bloomberg News had expected headline CPI to print at 0.1% m/m and 3.3% y/y.

Excluding food and energy, so-called core CPI, intended to reveal longer-term economic trends while minimizing data fluctuations caused by the volatility of some items in the typical consumer’s basket, increased 0.2 % m/m, surprising to the downside by one-tenth of a percent. Compared with one year ago, the underlying gauge grew by 4.2%, a step down from September’s 4.3% advance.

Overall, inflationary forces are moderating, but the process is clearly slow and painful for consumers. Today’s report, however, should reinforce the Fed’s decision to proceed carefully, reducing the likelihood of further tightening during this cycle. The data may also give officials the cover they need to start embracing a less aggressive posture – an outcome that could weigh on U.S. yields and, therefore, the U.S. dollar. This could be positive for gold prices.

Eager to gain insights into gold’s future path and the catalysts that could spark volatility? Discover the answers in our Q4 trading forecast. Get the free guide now!

Recommended by Diego Colman

Get Your Free Gold Forecast

US INFLATION RESULTS

Source: DailyFX Economic Calendar

INFLATION CHART

Source: BLS

Will the U.S. dollar extend higher or reverse lower in the near term? Get all the answers in our Q4 forecast. Download the trading guide now!

Recommended by Diego Colman

Get Your Free USD Forecast

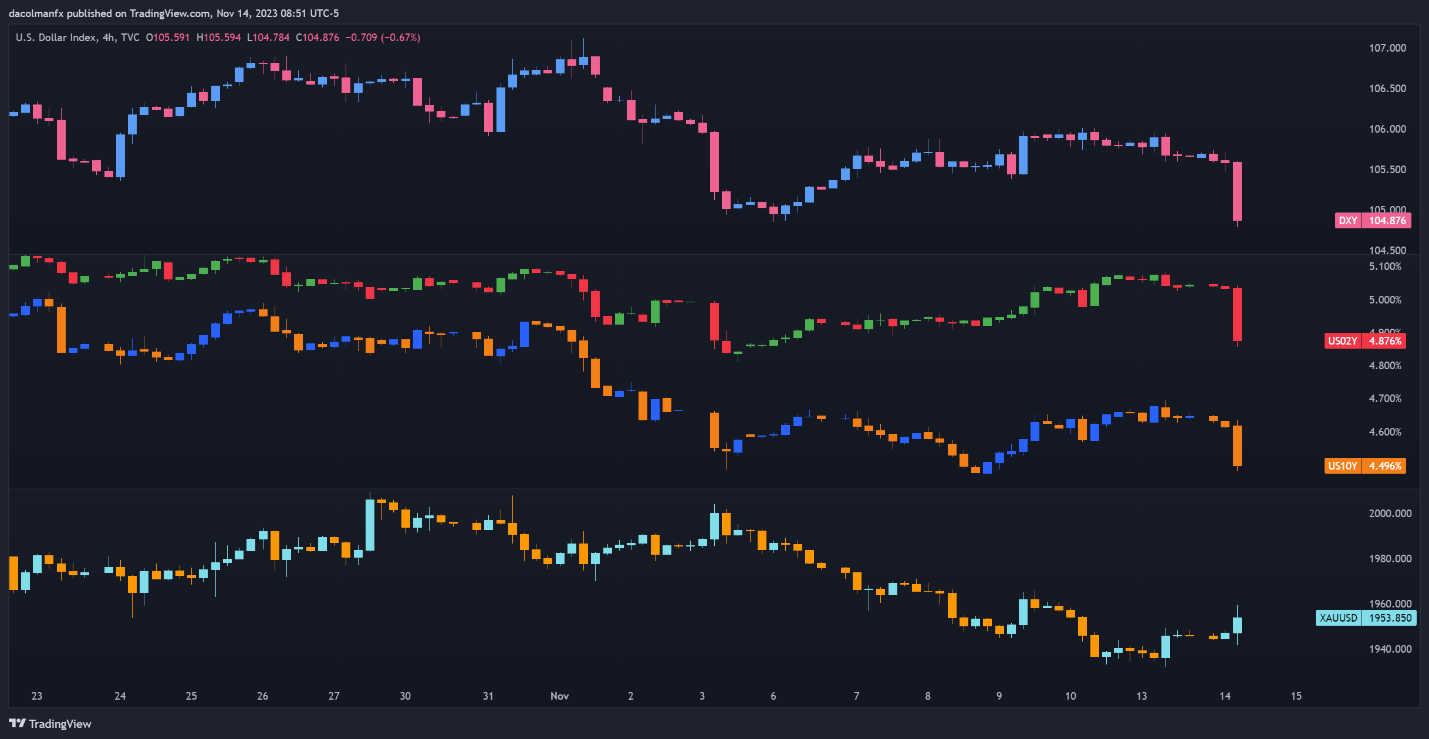

Immediately after the CPI report was released, the U.S. dollar, as measured by the DXY index, took a tumble, sinking more than 0.7% on the day, dragged lower by the steep downturn in U.S. Treasury yields. Meanwhile, gold prices advanced, climbing about 0.5% in early trading in New York.

Benign inflation numbers, if sustained, should weigh on rates heading into 2024. This could create the right conditions for a sharp downward correction in the U.S. dollar, which would stand to benefit precious metals such as gold and silver.

MARKET REACTION – US DOLLAR, YIELDS AND GOLD

Source: TradingView

Read the full article here

Warning: Team Sounds the Alarm")